{kind=link}

Submitted by QTR’s Fringe Finance

“This time it’s different” is supposed to be the dumbest phrase in investing.

It’s the phrase people use right before they get obliterated. It was the rallying cry of dot-com lunatics buying companies with no revenue in 1999. It was the intellectual foundation of housing perma-bulls in 2006 who believed home prices could only go up because, apparently, Americans had collectively decided real estate was immune mathematical reality.

It’s typically what people say when they’re trying to justify paying absurd prices for dogshit assets while pretending the laws of valuation have been permanently repealed: “this time it’s different”.

Which is why it’s deeply annoying and borderline humiliating for me to admit that this time, it actually may be different.

As someone who has spent years living in the world of fundamentals, valuation discipline, and the radical idea that cash flows should matter at least a little when valuing businesses, I hate where the evidence keeps leading me. I’ve spent years mocking the market as distorted.

Everyone in Austrian economics circles loves that word: distorted. Markets are distorted by central banks, distorted by artificially low interest rates, distorted by endless intervention. Distorted, distorted, distorted. Fine. But at some point, if a distortion lasts long enough, survives every crisis, and becomes embedded in how markets function, is it still a distortion? Or is it just the market now?

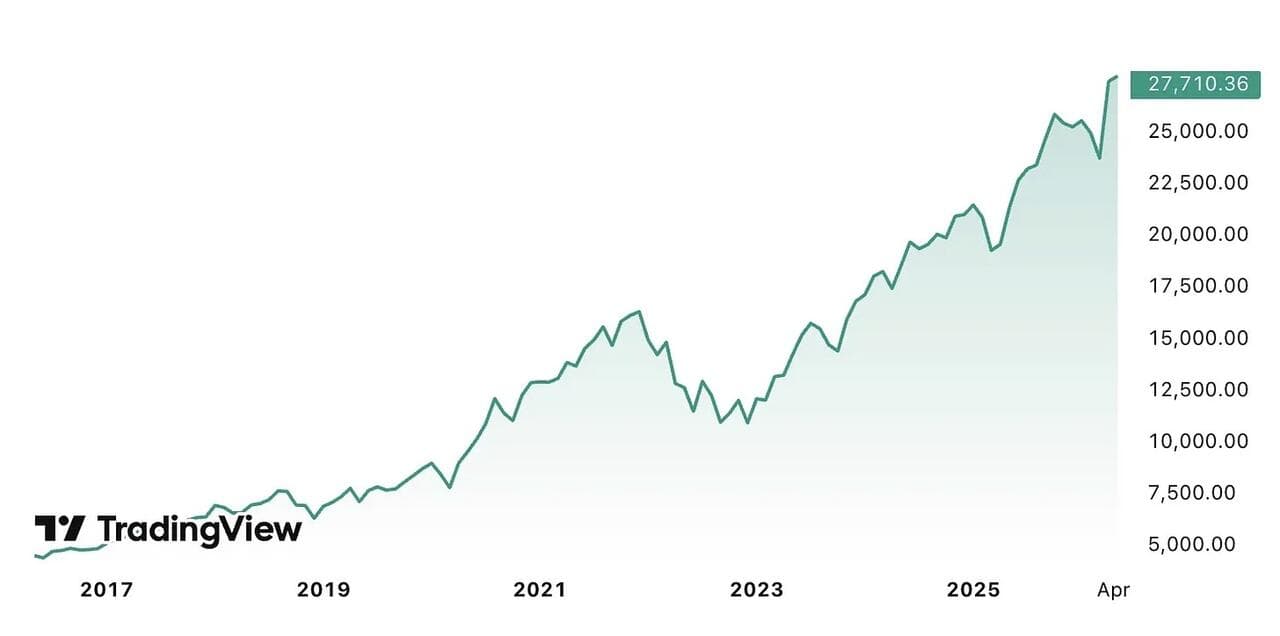

Look at this chart of the NASDAQ tripling off Covid lows just 5 years ago before you answer. An index. Tripling.

And in ten years, the index (read it again, index) is up 534%.

And now, back to the question: “if a distortion lasts long enough, survives every crisis, and becomes embedded in how markets function, is it still a distortion?”

That’s the uncomfortable question fundamental investors increasingly refuse to confront. We continue dragging out valuation charts that go back to 1900 as if they’re sacred scripture. We point to historical average P/E ratios and the Buffett Indicator and say things like “the market has always reverted.”

I’ve said such things on this blog for years.

But the market that existed in (throw a dart) 1952 has almost nothing in common with the one we have today. Back then there were no ETFs mechanically absorbing retirement contributions every two weeks regardless of valuation. There was no passive investing machine blindly funneling trillions into the largest companies simply because they’re already the largest companies. There were no options markets large enough to create absurd gamma-driven price movements detached from fundamentals. There were no retail armies weaponizing leverage from their phones while posting rocket ship emojis.

And there sure as hell was no widely accepted assumption that if markets fall hard enough (3%, give or take a percent?), the Federal Reserve will eventually arrive with fresh liquidity and soothing words about financial stability.

For fifteen years, investors have been trained like goddamn lab rats to expect intervention whenever things get ugly enough. In 2008, the financial system nearly collapsed and the response was unprecedented monetary intervention. In 2020, the world shut down and trillions appeared almost overnight. Every time markets experience genuine pain, policymakers magically “discover” yet another reason why extraordinary intervention is necessary.

The lab rats participating in this market have learned a very simple lesson: the adults will not tolerate prolonged asset deflation. They may talk tough about inflation. They may posture about financial discipline. But when enough things start breaking, they fold. They always fold.

Markets now operate with the deeply embedded belief that liquidity will always return when things get sufficiently bad. That belief alone changes behavior. It encourages risk-taking. It compresses risk premiums. It makes traditional valuation frameworks feel increasingly obsolete because those frameworks were built during periods when markets still had to fully purge excesses. Today, excesses are often interrupted, softened, or reflated before true cleansing can occur.

Meanwhile, people love pretending the stock market’s relentless rise is purely a reflection of corporate innovation and productivity gains. Some of it absolutely is. But a meaningful portion of what investors celebrate as “wealth creation” is simply the declining purchasing power of the currency in which those assets are priced. If you continually debase the measuring stick, asset prices are going to look fantastic. Stocks haven’t always become more valuable. Dollars have become less valuable.

If your denominator is quietly melting, your numerator tends to look heroic. It can even make the performance of an ex-bartender from Philadelphia writing a finance blog look great.

This forces an almost heretical conclusion I’ve been toying with for a year or two: maybe what we consider “expensive” is anchored to a market regime that no longer exists. Maybe 20x earnings is not expensive anymore because 20 years of future earnings are guaranteed in a way they weren’t 50 years ago. Maybe for dominant, cash-generating businesses, 20x is the new bargain bin. Maybe historical comparisons to decades that lacked passive flows, algorithmic trading, derivatives-fueled volatility, trillion-dollar buybacks, and perpetual monetary intervention are becoming less useful by the year.

🔥 50% OFF FOR LIFE: Using this coupon entitles you to 50% off an annual subscription to Fringe Finance for life: Get 50% off forever

I can already hear the response. Shit like “this article really must mean the top is in” and “QTR has caved, we can crash now!” Look, of course valuation still matters. Gravity still exists too. But if central banks keep dropping trampolines underneath the market every time gravity starts doing its job, people should stop acting shocked when assets bounce higher than historical models suggest they should.

This doesn’t mean crashes disappear. Something will absolutely break eventually, and probably the moves lower will be sharper and faster, before they aren’t, because that’s what leveraged systems do. But each break seems to justify larger interventions, which creates even bigger distortions, which produce even larger asset bubbles, which eventually require even more intervention. It’s a magnificent ouroboros of financial engineering and moral hazard.

And that’s the truly infuriating part for people like me. I want old valuation frameworks to still work cleanly. I want patient fundamental analysis to feel like an advantage rather than a history hobby. I want “cheap” and “expensive” to retain actual meaning. But markets increasingly feel like they’re operating under a new regime where liquidity overwhelms nearly everything else over long enough time horizons.

“This time it’s different” remains a dangerous phrase because human beings are still perfectly capable of creating idiotic bubbles. But pretending this market functions like the one our grandparents invested in may be its own form of delusion.

If the Fed has effectively made permanent distortion the foundation of modern markets—and if it cannot stop until something truly catastrophic breaks—then maybe we need to admit the obvious: the market is no longer broken. It’s functioning exactly as designed: rigged.

But of course, now that I’ve penned and published this piece, a medieval-style return to the investing dark ages is probably right around the corner.

Now read:

- Congrats, Elizabeth Warren, On The Death Of Spirit Airlines

- Buying One Staple Stock That’s Been Crushed

- Stocks Now In “The Biggest Bubble Of Modern Times”

- Glowing Numbers…With Glaring Omissions

—

QTR’s Disclaimer: Please read my full legal disclaimer on my About page here. This post represents my opinions only. In addition, please understand I am an idiot and often get things wrong and lose money. I may own or transact in any names mentioned in this piece at any time without warning. Contributor posts and aggregated posts have been hand selected by me, have not been fact checked and are the opinions of their authors. They are either submitted to QTR by their author, reprinted under a Creative Commons license with my best effort to uphold what the license asks, or with the permission of the author.

This is not a recommendation to buy or sell any stocks or securities, just my opinions. I often lose money on positions I trade/invest in. I may add any name mentioned in this article and sell any name mentioned in this piece at any time, without further warning. None of this is a solicitation to buy or sell securities. I may or may not own names I write about and are watching. Sometimes I’m bullish without owning things, sometimes I’m bearish and do own things. Just assume my positions could be exactly the opposite of what you think they are just in case. If I’m long I could quickly be short and vice versa. I won’t update my positions. All positions can change immediately as soon as I publish this, with or without notice and at any point I can be long, short or neutral on any position. You are on your own. Do not make decisions based on my blog. I exist on the fringe. If you see numbers and calculations of any sort, assume they are wrong and double check them. I failed Algebra in 8th grade and topped off my high school math accolades by getting a D- in remedial Calculus my senior year, before becoming an English major in college so I could bullshit my way through things easier.

The publisher does not guarantee the accuracy or completeness of the information provided in this page. These are not the opinions of any of my employers, partners, or associates. I did my best to be honest about my disclosures but can’t guarantee I am right; I write these posts after a couple beers sometimes. I edit after my posts are published because I’m impatient and lazy, so if you see a typo, check back in a half hour. Also, I just straight up get shit wrong a lot. I mention it twice because it’s that important.