{kind=link}

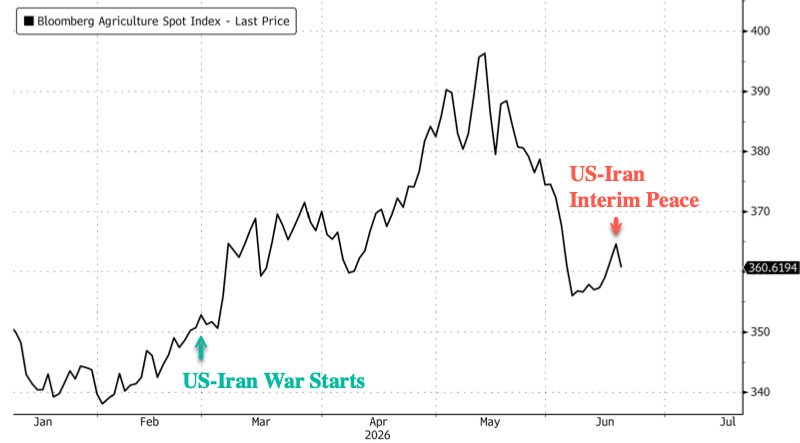

The Bloomberg Agriculture Spot Index has nearly reversed its US-Iran war gains in recent weeks, as sliding fertilizer and energy prices, along with an interim peace deal between Washington and Tehran, have reopened the Strait of Hormuz and initiated the normalization process.

Daryna Kovalska, a commodity strategist at BofA Global Research, told clients that, with agricultural markets having undergone an aggressive positioning washout, there is reason to believe the selloff in the corn market is overdone.

Kovalska pointed out that while improved US rains, easing geopolitical risks, and lower urea prices have stripped weather and war premiums from the market, her team believes risks have been deferred rather than eliminated. She remains constructive on corn, while trimming its 2026 upside target to $5.50 per bushel from $6.00.

More color here from her note titled “Corn market cools, but risks simmer beneath“:

Ag markets hit by sharp spec long liquidation…

Agricultural markets have undergone an aggressive positioning washout, with net spec longs down 88% in three weeks. Corn hasn’t been spared: managed money flipped from decade-high longs to a net short by June 9, sending Dec 26 prices to a low of $4.4/bu.

…but we believe the corn selloff is overdone

Corn sentiment has softened, as geopolitical and weather risks have eased. But risks have not disappeared; rather, they look deferred and could still trigger a supply shock. We remain constructive, though, trimming our 2026 upside to $5.5/bu from $6.0/bu, supported by three key arguments.

1: Weather risk premium has been stripped out too early…

Improved US rains have eased weather risks in the corn market, but threats persist in certain states. Nebraska (12% of US production) remains in severe drought, with crop conditions 20% below average, while South Dakota and Kansas ratings (another 12% of output) are at risk of deteriorating without sustained rainfall.

…especially with an unprecedented El Nino unfolding

The Australian Bureau of Meteorology continues to warn of an historic El Niño event. Brazil’s corn output could be hit hard, declining 10% yoy in 2026/27E. Iowa state also shows a pattern of sharply depleted soil moisture during analogues.

2: Brazil fertilizer supply remains a concern

Urea prices have eased, but despite a potential US-Iran deal to be signed on June 19, the Strait of Hormuz still needs to be de-mined and resume operations, with timing critical as Brazil’s peak dispatch window approaches. Substitution efforts remain insufficient, with nitrogen imports still down 15% yoy, putting first crop corn yields at risk of a 10% decline if Gulf urea shipments do not restart before the end of July. Phosphate constraints are compounding risks to the new crop, which could fall 10 mn t yoy.

3: US-China $17bn deal could upend the market

The White House expects China to buy at least $17bn of US ags annually in 2026 (pro- rated) and 2027-28. Mirroring Phase One, we think US corn exports to China could surge from zero in 2025 to 5.5 mn t in 2026 and 16 mn t thereafter. While purchases have yet to begin, implementation would materially tighten the US corn market.

Kovalska provides her team’s view from macro to crude to softs:

Here’s her price forecasts across softs:

With the war-risk premium evaporating from agricultural markets, Kovalska believes that lingering risks around weather, fertilizer flows, El Niño, and Chinese demand could still combine to tighten global supply and push prices higher again.